- TheoTrade (FOMO)

- Posts

- This Is Always The Easiest Short

This Is Always The Easiest Short

Death, Taxes, And This Product Going To Zero.

Don Kaufman

April 22, 2026

Somebody mentioned UVXY in the chat yesterday.

Bad idea.

Not because it is a bad trade right now. Because it is always a bad trade. And I know this not me being negative.

I know it because I sat across from the people it destroyed.

Fifteen and zero.

That was my record as an expert witness for TD Ameritrade. Every time a client sued over a volatility product that went to zero, they brought me in.

Suit, no tie, and always caffeinated. I Spoke slowly because the attorneys were billing $1,200 an hour and I did not care.

The cases were almost always the same.

Someone put serious money into TVIX. TVIX went to near zero. They sued.

I sat across from them and asked one question.

At any point in the three years you owned TVIX, did you not realize that TVIX always goes down?

The answer was almost always no.

So let me explain what these products actually are, because most people who trade them have no idea.

TVIX, UVXY, and VXX are not volatility products. They do not track the VIX. They track VIX futures.

Specifically, they hold the two nearest VIX futures contracts and roll them forward every single day. That distinction is the entire ballgame and almost nobody understands it before they put money in.

Here is why it matters.

VIX futures, in normal market conditions, trade in contango. Contango means the futures contracts further out in time are priced higher than the contracts closest to expiration. Every single day, these products have to sell the expiring contract and buy the next one further out.

Sells low. Buys high. Every day.

Mechanically. That roll cost eats the product alive.

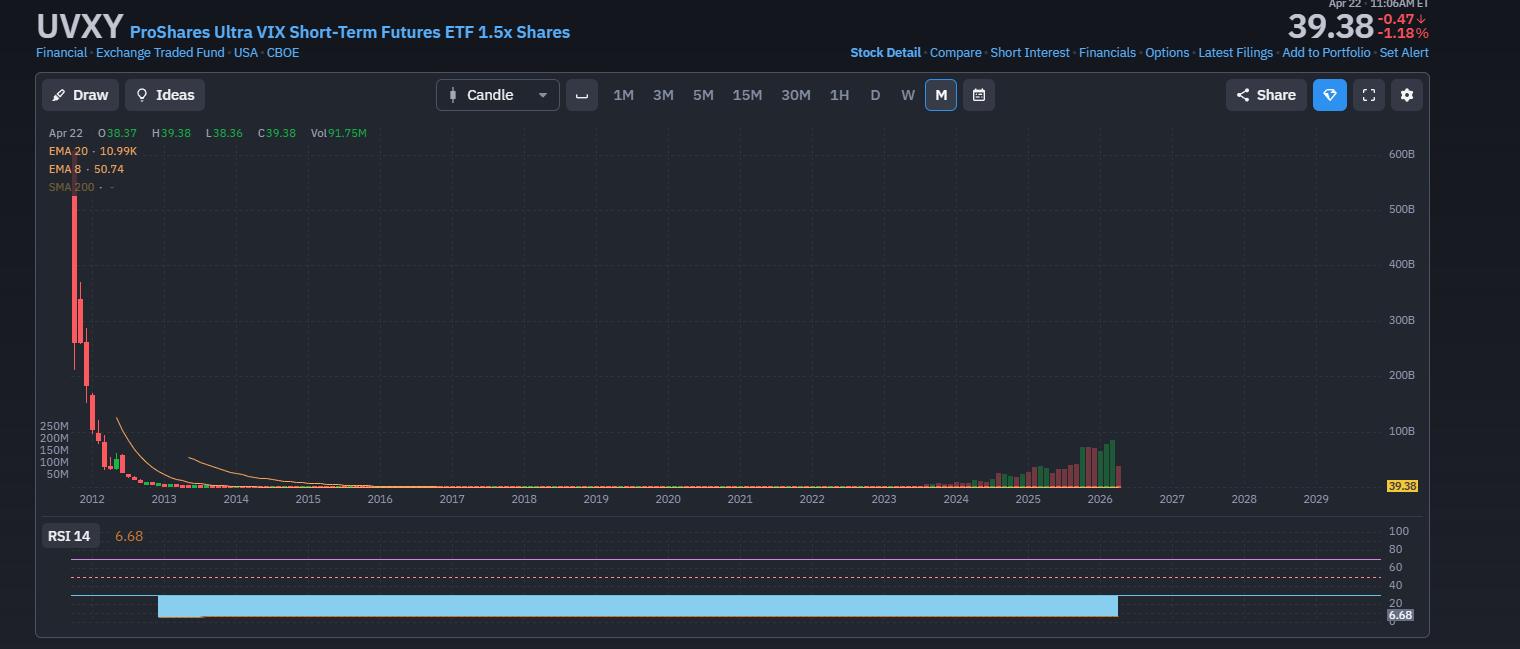

The decay numbers are not small. In normal conditions, contango eats UVXY at a rate of 50 to 85 percent per year depending on leverage.

A share of UVXY bought at inception in 2011 for $40 would be worth less than 0.0001 cents today if the fund did not reverse split to keep the share price alive.

VXX has reverse split eight times for the same reason. TVIX decayed all the way to 19 cents per share before Credit Suisse shut it down entirely.

None of this has anything to do with what volatility actually does. It does not matter if the VIX spikes or stays flat. The roll cost runs every single day.

The chart always goes down and to the right over any meaningful holding period.

That is what I was explaining in those arbitration rooms. The product was not fraudulent. It worked exactly as designed.

The problem was that nobody buying it understood what it was designed to do.

So what do I use when I want exposure to volatility?

VIX options. Specifically because they are cash settled. Cash settled means when the option expires, the difference is paid out in cash. No underlying shares to be assigned.

No futures rolling against you in the background. No structural decay eating your position while you wait.

VIX options do have quirks and I want to be straight with you. They expire on a Wednesday morning on AM settlement.

Last time you can trade them is Tuesday afternoon.

The expiration structure looks nothing like any standardized equity option. And they trade like a commodity, not like a stock option, because that is exactly what they are.

But they are liquid. The open interest is real. And when you take a position in VIX options, you are actually taking a position on volatility.

Not on a product that is quietly rolling futures against you every single day while you watch the chart head toward zero.

The traders in those arbitration rooms had neither the framework nor the trade.

They had a ticker and a chart they never looked at.

To your success,

Don Kaufman

P.S. Judgement Day is here. Will you be ready?